The Market Finally Gets Its Wish

The Fed starts easing cycle with a bang.

The bulls raged on Thursday following the commencement of the Federal Reserve’s latest rate cutting cycle, with the S & P 500 rising 1.7% to a new all-time high, before easing back a bit on Friday. After two years of markets pricing in rate cuts, the central bank finally saw enough economic risk to make the dream come true. Conventional wisdom is that rate cuts are always good news for the economy and markets, but history is less definitive.

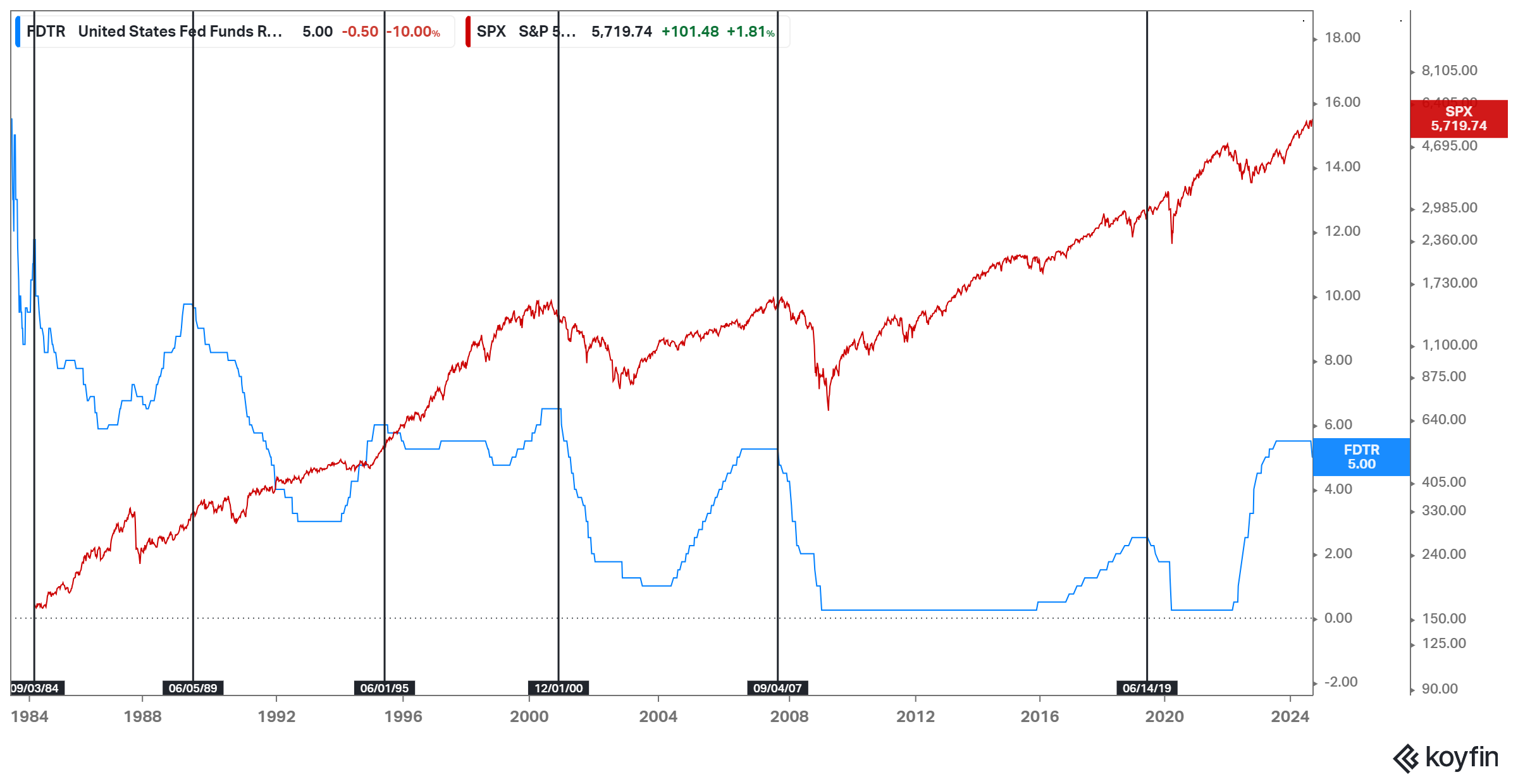

It is true that markets usually rise within 12 months of the beginning of an easing cycle, but there have been major exceptions, and much depends on the economic backdrop. Below is a chart of the S & P 500 (red) overlayed with the Federal Reserve Target Rate (blue) back to 1981. The black vertical lines designate the beginning of rate cutting cycles.

One noticeable thing from this chart is that the three rate cut cycles between 1981 and 2000 all led to substantial bull moves higher in stocks. Many would consider this period the biggest “secular bull market” in U.S. history, as stocks went from record low valuations to record high valuations over the span. Double digit interest rates from the early ‘80s, along with single digit P/E ratios, were a major tailwind for stocks throughout that period.

At the turn of the millennium, the backdrop shifted drastically, with sky high equity valuations, and more normalized interest rates. The beginning of the next two rate cut cycles (2000 and 2007) both served as omens of more challenging times to come, as they preceded nasty bear markets, and in the case of 2007, a severe financial crisis. However, 2020 is more difficult to analyze. The market initially went higher, but Covid soon shut down the entire world, and markets went into a tailspin.

Thursday’s sharp rally notwithstanding, it’s too early to know whether Wednesday’s 50 basis point cut will be the start of a prolonged rate cutting cycle, or whether it will fuel another major leg up in this bull market. What we do know is economic data has shown enough weakness to spur the Fed to action, and that’s not always a buy signal. The Fed sets the marginal cost for credit with its policy rate, but that’s only half the story in recent years. Quantitative easing, or tightening, is just as important. I’ll touch upon QE and QT in my next post, along with its broader implications.